In a remarkable turn of events, a Pennsylvania family stumbled upon a rare 1964 Kennedy half dollar coin while sorting through their grandfather’s vintage items.

Initially overlooked among the tools and trinkets, this coin has now been appraised at over $50,000, captivating the attention of coin collectors and enthusiasts alike.

The Discovery

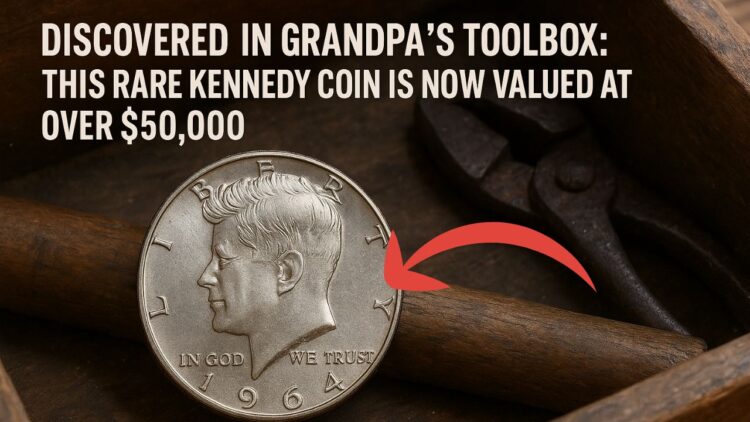

During a routine spring cleaning session, a family in Pennsylvania uncovered a 1964 Kennedy half dollar hidden amidst their grandfather’s mechanic tools.

At first glance, it appeared to be a typical coin from the era. However, upon closer inspection, it was revealed to be a rare variant with a significant minting error, making it a highly sought-after collector’s item.

Historical Background of the 1964 Kennedy Half Dollar

The Kennedy half dollar was introduced in 1964, just months after the assassination of President John F. Kennedy. The U.S. Mint replaced the Benjamin Franklin half dollar with a new design featuring Kennedy’s profile, serving as a tribute to the late president.

Struck in 90% silver, millions of these coins were minted that year, making them a significant part of American numismatic history.

The Unique Minting Error: Double Die Obverse

The coin discovered in the toolbox is a 1964-D Kennedy half dollar exhibiting a rare minting error known as a “double die obverse.”

This error occurs when the coin’s design is struck twice by the die, resulting in a noticeable doubling effect on the inscriptions and images on the obverse (front) side of the coin. Such errors are uncommon and significantly enhance the coin’s value among collectors.

Factors Contributing to the Coin’s High Value

Several elements contribute to the substantial value of this particular coin:

- Minting Error: The double die obverse error is a significant factor, as it is rare and highly valued in the numismatic community.

- Historical Significance: Being part of the first series minted after President Kennedy’s assassination adds historical value.

- Silver Content: The coin’s composition of 90% silver increases its intrinsic value.

- Condition: The coin’s well-preserved state further elevates its desirability among collectors.

Identifying Valuable Coins

For those interested in identifying potentially valuable coins, consider the following tips:

- Examine Mint Marks: Small letters on the coin indicate the U.S. Mint location where it was produced.

- Check for Minting Errors: Look for anomalies such as double strikes, off-center impressions, or missing elements.

- Assess Condition: Coins in pristine condition are more valuable.

- Research Rarity: Limited mintage and unique features can increase a coin’s worth.

For accurate valuation and authentication, consulting with professional coin grading services is recommended.

Key Information of the 1964 Kennedy Half Dollar

| Feature | Details |

|---|---|

| Year Minted | 1964 |

| Mint Mark | D (Denver) |

| Composition | 90% Silver, 10% Copper |

| Diameter | 30.6 mm |

| Weight | 12.5 grams |

| Minting Error | Double Die Obverse |

| Estimated Value | Over $50,000 |

| Historical Context | First series minted post-President Kennedy’s assassination |

| Collectibility | High due to rarity and condition |

The discovery of the rare 1964 Kennedy half-dollar coin in a grandfather’s toolbox serves as a testament to the hidden treasures that may lie within everyday items.

This incident highlights the importance of carefully examining old coins, as they may possess significant historical and monetary value. For collectors and enthusiasts, this story underscores the excitement and potential rewards of the numismatic world.

FAQs

How do I apply for the BC Family Benefit?

You do not need to apply separately. If you’re eligible and have filed your taxes, the CRA will automatically issue payments.

Can I receive both the BC Family Benefit and Canada Child Benefit (CCB)?

Yes, both benefits can be received simultaneously, providing increased monthly support for eligible families.

What if my income changes mid-year?

The CRA assesses benefit amounts annually based on your tax return. Significant changes may affect next year’s benefit, but not current payments.